Confronted with a huge fiscal gap, elevated prices and the threat of economic recession, the former government chose to solve the problems by large tax cuts, instead of the unpopular austerity moves for fiscal consolidation. Unfortunately, the financial markets did not appreciate it. They were worried about where money came from and the unsustainable deficit. The UK government bonds market was in turmoil. The liquidity crisis of pension funds was triggered. GBP/USD hit a record low of 1.0284 on September 26 this year, less than 300 points reaching the important psychological level of one to one.

The Bank of England intervened in time to buy public bonds unlimitedly for a certain period of time to relieve panic. The exchange rate of the pound rebounded sharply to around 1.15 US dollar. Liz Truss became the shortest-serving Prime Minister of the United Kingdom. She resigned after 45 days in office, and her tax cuts came to an end. Another negative factor for the pound is fading. US inflation is slowing down, and the market begins to speculate that the US interest rate hike cycle is coming to an end. The US dollar fell broadly, and GBP/USD rebounded above the level of $1.20.

What caused the pound to fall and threaten 1 US dollar level was a crisis, which was the liquidity crisis of pension funds. Crises usually cause panic, leading to unusual levels of asset prices. Therefore, another crisis is needed to a large extent for GBP/USD to attack the defence line of 1.0000 again.

Some analysts believe that the UK is sliding into the debt financing crisis. The Bank of England is selling British public bonds, reducing the £835 billion bonds accumulated in quantitative easing policies for more than a decade, and the £19 billion Gilts purchased at the bailout in September. When the supply of public bonds continues to rise, and the central bank keeps raising interest rates against inflation, financial markets may require higher returns for them to buy Gilts. If the debt issuance of the Ministry of Finance turns out poorly demanded, will the bond markets fluctuate dramatically again?

The difference is that the new government has decided to restore its fiscal credibility in a positive way. Rishi Sunak's government will raise taxes and reduce fiscal expenditures in the next few years to fill the budget deficit of up to 55 billion pounds. This is a painful but correct path, bringing hope to a sound finance and economic recovery in the future. Therefore, it may be a bit over-worried to say it is a crisis, despite the pressure of debt financing.

Many people are doubtful why the Federal Reserve has raised interest rates like crazy, ignoring its economy may fall into recession, which brings so much pressure to the global economy. The Federal Reserve's strategy is to scare inflation down by a super hawkish stance. If it succeeds, the peak of this interest rate hike cycle will be lower than expected. Even if the economy falls into recession, it will last for a shorter period.

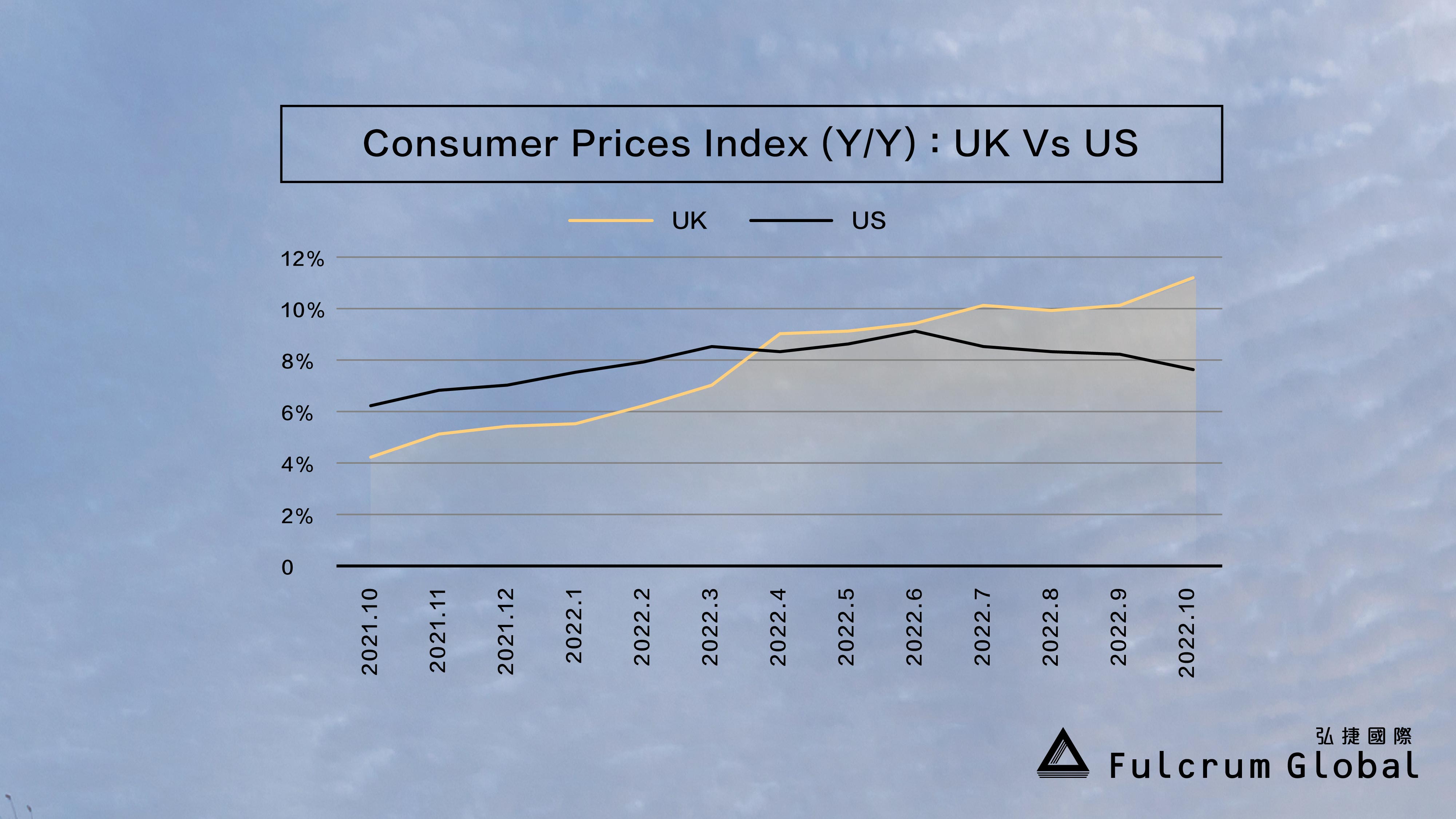

The US consumer price index slowed down to 7.7% in October, the lowest since January this year. The financial markets are very excited. They not only speculate that the Federal Reserve will slow down the pace of raising interest rates, but also estimate that the interest rate hike cycle is coming to an end. The U.S. dollar has fallen widely, and the stock market rebounds. Federal Reserve officials are divided. Some begins to worry about excessive austerity and deepening the recession. We will see the hawkish to insist on fighting inflation strongly. However, if inflation data show more slowdown trends, the voice of the pro-growth camp will be louder.

The rebound of GBP/USD from 1.0284 is still continuing, but this rebound mainly depends on the diminishing bad news. More troublesome is that the short-term fundamentals of the pound are unfavourable. The attempt of GBP/USD to rise above 1.25 to 1.30 zone will meet with resistance. In order to improve the medium-term technical prospects, the new downward trend after this rebound should fail to challenge 1.0284.

The short-term outlook for the British economy is not optimistic. UK inflation rose to a 41-year high of 11.1% in October. The British interest rate is expected to reach 4.5% next year and will remain until the end of 2023. The OBR predicts that the British economy will fall into a recession for over a year from the third quarter of this year. The economy will shrink by 1.4% in 2023, and inflation will fall back to 7.4% from 9.1% this year, still far higher than the central bank's target of 2%.

The spending cuts plan of the British government will not take effect until after the 2024 general election. What is the government waiting for? Since the U.S. inflation has reached an inflection point, British inflation may also begin to slow down in the short term. If the weakening of inflation in the UK is better than expected, the central bank will not raise interest rates so much. The cost of debt interest will be lower, and fiscal austerity will not be so radical.

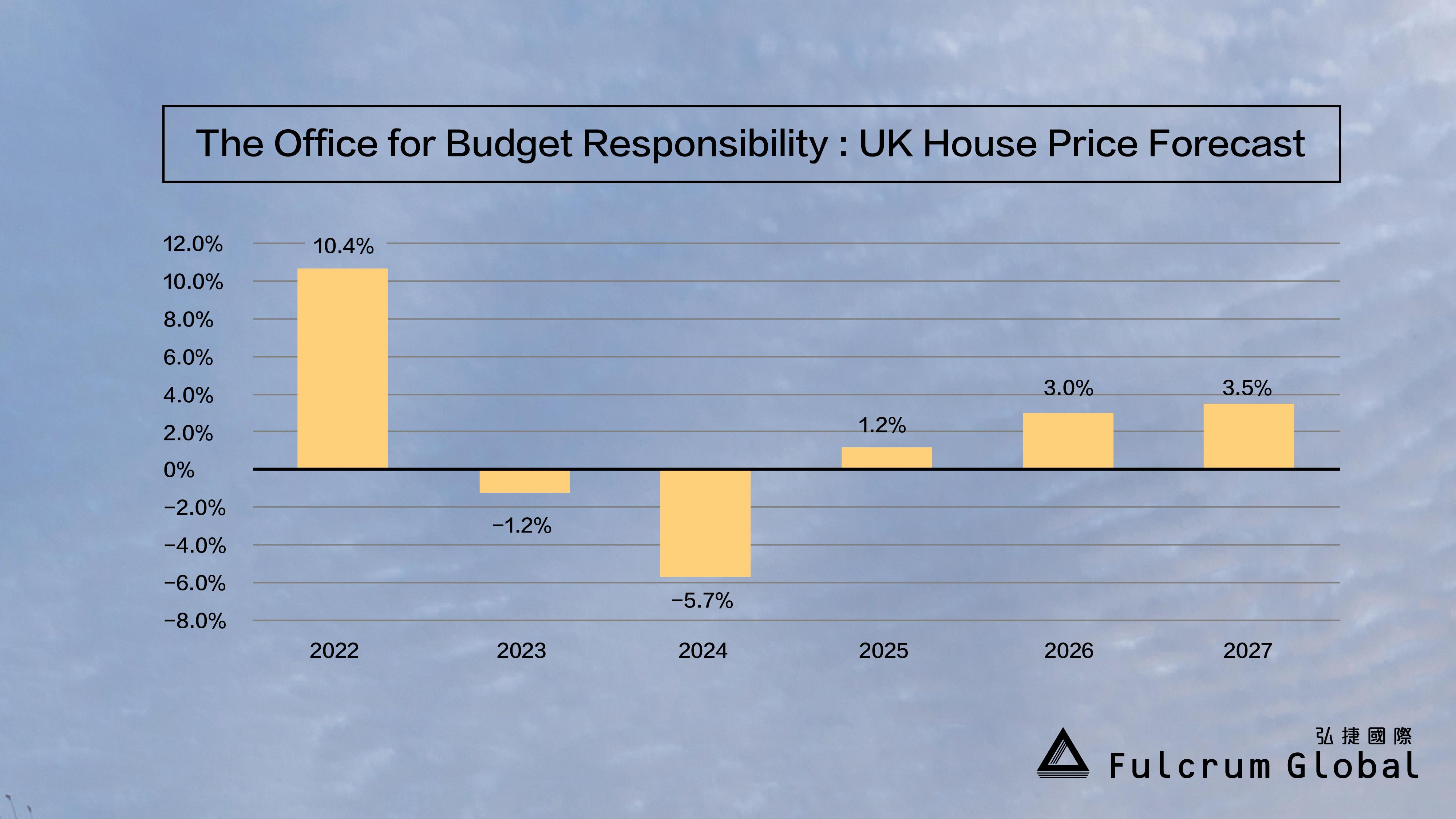

The downward adjustment of housing prices in the UK may be very limited, despite pressured by economic contraction and rising mortgage interest rates. The OBR predicts that after rising by 10.7% this year, housing prices will fall by 1.2% in 2023 and 5.7% in 2024, and then return to the upward trend.

The British rental market is still very tense. According to Rightmove's third quarter data, monthly rents outside London reached a record high of £1,162, an annual growth rate of 11%; the monthly rent of houses in London rose to £2,343, an annual growth rate of 16.1%. Rightmove pointed out that the demand for tenants increased by 20% compared with last year, but the supply of available rental housing decreased by 9%. According to RICs' residential market survey, the October tenant index reported +46%, and the landlord index was -14%.

The rise in mortgage interest rates weakens affordability. Whether house prices will fall in the next two years will encourage wait and see. First time home buyers tend to continue to rent a house. Although government data show that the housing supply increased by 232,820 units from 2021 to 2022, an increase of 10% from 2020 to 2021, the data is actually weak because the housing supply decreased by 13% during the COVID-19 pandemic. The housing shortage is still very serious. According to the research of Heriot-Watt University, at least 340,000 new houses are needed to be built in the UK every year, of which 145,000 units must be affordable and need to last until 2031, because the shortage of 4 million units in the UK.

The UK housing rents will maintain an upward trend but two points need attention. The strong rising path of rent may be slightly slowdown. RICs expects national rents to rise by about 4% in the next 12 months. London's rent rising trend shows signs of overheating, and the average rent as a proportion of the total income of tenants has risen to 52%, much higher than 37% outside London. Strong demand but subject to affordability, more tends to look for rental listings outside London and narrow the rent gap between London and other regions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}